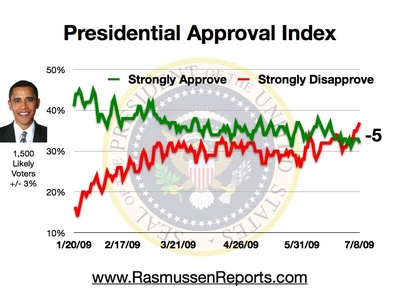

The Rasmussen Reports daily Presidential Tracking Poll for Wednesday shows that 32% of the nation's voters now Strongly Approve of the way that Barack Obama is performing his role as President. Thirty-seven percent (37%) Strongly Disapprove giving Obama a Presidential Approval Index rating of –5.

The number who strongly disapprove inched up another point to the highest level measured to date and the overall Approval Index is at the lowest level yet for Obama...

Why Unemployment Could Hit 14%.

The Labor Market Is Worse Than You Think.

U.S. Workers Hired at Slowest Rate in 9 Years.

Stocks Hit 10-Week Low.

Consumer Loan Delinquencies Rise to Record Levels.

The key here is to realize who is responsible: Barack Obama. He's still trying to pass the buck to George W. Bush, but the fact is that Obama and the Democrats are the ones who've spent trillions of dollars in just five months, exploding the deficit and national debt, and burying multiple generations of as-yet-unborn Americans under massive financial obligations. The question of who is responsible is the crux of the matter, and it needs to be squarely confronted and explained truthfully.

Also on the decline is another key economic indicator, consumer confidence:

Bottom line: the Obama economy is failing.

(ABC News)

Consumer confidence is nearing a new record low.

Yid With Lid reported this from ABC News:

Consumer confidence is within striking distance of its worst in weekly polls since late 1985 for the third straight week.

The ABC News Consumer Comfort Index stands at -52 on its scale of +100 to -100, 2 points from the lowest on Jan. 25. The index has spent the last three weeks below -50, territory it's seen only 14 times in over 1,220 weeks of polls, with eight of those coming this year alone.

Celebrating his first 100 days in office, President Barack Obama told the American people: "One hundred days ago, in the midst of the worst economic crisis in half a century, we passed the most sweeping economic recovery act in history…One hundred days later, we are already seeing results." And he's right, we are. Unemployment has risen to 9.5%, stocks fell to their lowest level in 10 weeks on Tuesday, and consumer credit delinquencies have hit a record high. Responding to the obvious failure of the Obama administration's $787 billion stimulus package, some liberals in the House and Senate are calling for a second (really the third when you count President Bush's 2008 effort) stimulus. How big of a second stimulus? Center for Economic and Policy Research co-director Dean Baker told Politico: "To my mind it's pretty obvious we need another stimulus package, probably a lot bigger than the last one."

To be fair, the Obama administration itself is not yet ready to admit their first $787 billion stimulus package failed. Both Vice President Joe Biden and Obama Council of Economic Advisers member Austan Goolsbee recently said it was premature to discuss crafting another stimulus. But outside adviser to President Obama Laura Tyson told an audience in Singapore yesterday that the stimulus package was indeed "a bit too small" and that the administration should consider a second effort. According to Bloomberg, Tyson then stressed "The U.S. needs to communicate its determination to reduce the annual shortfall once the economy recovers." Unfortunately the Obama administration is sending no such credible signals.

The numbers don't lie, and here is the story they tell:Ignoring Obama's lofty rhetoric and focusing on the hard numbers, investors are demanding higher interest rates to soak up the tremendous flows of debt coming out of the Treasury. This will mean higher interest rates for consumer loans, mortgage loans, business loans, etc. The debt-based Obama economic stimulus plan has become a major drag on economic recovery, just as expected.

- Obama's "stimulus" bill alone will create more debt (approximately $1 trillion including interest costs), than Bush's first three years of budget deficits combined ($948 billion).

- Under Obama's budget, the national debt will increase by more in two years than it did under President Bush in eight years.

- Obama's spending will reach 24.5 percent of GDP, far higher than the post-war average of about 20.2 percent.

The President and the Congress must realize that world investors will not be swayed by new budget rules or other posturing. They want to see the economy strengthen while the deficit comes down now, and fast. The solution is to set aside all the new spending proposals and start cutting spending fast. Otherwise we're going to have double digit unemployment for a long time to come.

Clearly, the hope-n-change is starting to meet reality, and the American people aren't nearly as enthused about it now as they were in November. Unfulfilled promises, rising unemployment, and massive debt will do that.

Unfortunately, it's not going to get better quickly. I once heard an economist describe the American economy as a giant tanker ship with a very small rudder. It just takes a long time for changes of direction to become visible, and once they do, we often find we've over-corrected. Obama has changed direction so far to the left that now, as people are beginning to see the results, it is too late to stop it easily or quickly, and we'll have to deal with his over-correction. By the time we start feeling the full effects of all his spending -- not to mention the coming inflation -- it's going to get downright brutal, and we'll just have to gut through it as best we can.

The one hope we have left is the 2010 election - remember, only about 30-40% of the stimulus money is supposed to be spent by that time, so if the GOP gets back into power (and gets its head straight), they could put a stop to a lot of the worst spending that has already happened, and curtail everything going forward (since all spending bills are supposed to originate in the House). Hopefully it'll happen, and hopefully it'll be enough to stop the worst damage. After all, a scary near miss is far better than actually hitting the rocks.

There's my two cents.

No comments:

Post a Comment